2015 Guide to buying a home post Bankruptcy, Short Sale or Foreclosure

Table of Content

You can also find more information and the official guidelines for this program on the HUD.gov website. It will remain on your credit report for seven years from the date of the first default. After seven years, it will no longer appear, but it will lower your credit score.

Please provide us with any additional information you would like to share with us. A growing number of Americans are reaching that juncture after going into foreclosure early in the housing crisis. News Corp is a global, diversified media and information services company focused on creating and distributing authoritative and engaging content and other products and services. After receiving your outstanding dues, the lender will release all your documents in their possession, such as your Title Deed and other property-related documents. Upon receiving confirmation from your lender, you can finish repaying your outstanding Home Loan balance and notify your lender of the same. The calculator then provides you with the total foreclosure amount and the amount you can possibly save as Home Loan interest.

FHA loans

Borrowers in this scenario are sometimes called boomerang buyers or borrowers. When dealing with boomerang buyers, mortgage companies want to be sure that the borrower has handled the situation that caused the foreclosure and wonât repeat past mistakes. He says these loans are likely to have much higher interest rates than loans to those with excellent credit.

LendingTree does not include all lenders, savings products, or loan options available in the marketplace. LendingTree is compensated by companies on this site and this compensation may impact how and where offers appear on this site . It will depend on the lender’s minimum credit score requirement, which often is around 620.

Lender Verification and Documentation Requirements

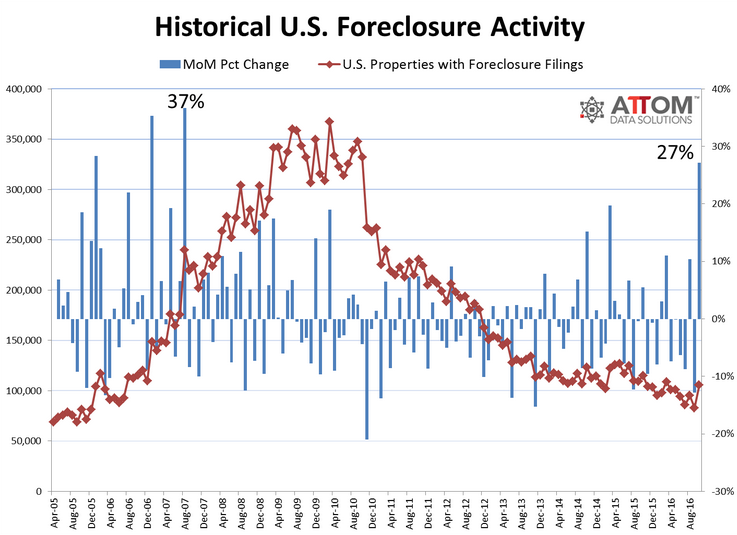

A foreclosure will result in the bank taking back ownership of the property and then bringing it to an auction. A short sale is when the house is sold before the house is foreclosed upon for a lesser amount than what is owed to the bank. Both cases will most likely affect your credit score for 7 years.

I had a client that wanted to buy a home in Arizona, but he had a foreclosure. After researching the web I found a loan program that allows a mortgage after a foreclosure. Since mortgage lenders review the last seven years of your credit history, it's a good idea to document in writing why you have a foreclosure on your credit report.

How to Get a Mortgage After a Foreclosure

The U.S. Department of Veterans Affairs guarantees VA loans for eligible military borrowers. In most cases, there’s no down payment required, though lenders may expect to see a minimum 620 credit score. Similar to FHA loans, extenuating circumstances are allowed for reasons “beyond the control” of the borrower if properly documented. The VA treats foreclosures similar to bankruptcies as well — at least one year of good credit is required for a VA loan eligibility. The FHA loan program does allow for documented extenuating circumstances, though it doesn’t specify an exact time frame.

But your interest rate will be several points over prime and you'll need 25% down. Keep in mind that Fannie Mae and Freddie Mac require private mortgage insurance for loans exceeding 80% of the property value or sales price. There is an important federal database known as the Credit Alert Verification Reporting System .

Loan Foreclosure Waiting Periods

After the auction, the new owner must notify the original owner of how long they can stay before eviction. In a judicial foreclosure, the lender files a lawsuit with the court, and a judge must approve the foreclosure before the lender schedules the property for auction. Judicial and non-judicial foreclosure also allows the lender to sell the property for less than the amount owed. However, lenders will inform you of the next steps, such as when the property will be scheduled for auction and when the foreclosure is expected to finalize. Temporary and permanent loan modifications are acceptable, as long as the payments have been documented and made on time in accordance with the modification agreement.

Accounting for 30 percent of your score, your outstanding debt may prove easier to clean up than your payment history. A large amount of debt can depress your credit score, so whittling away the amount you owe is key to improving your score. FOUR Years from short sale or deed in lieu of foreclosure with Maximum 80% Loan to Value. Communicating with your lender is always the best course of action since most lenders are willing to cooperate with borrowers to avoid the costly, time-consuming foreclosure process. The borrower’s credit report does not show any late payments on mortgage or revolving credit accounts. If you think your foreclosure was mismanaged by the lending bank then you might be able to get the foreclosure cleared from your credit report.

Many things can severely impact your finances, but most wonât qualify as extenuating circumstances. For example, going through a divorce or not being able to sell your real estate may seriously impact your finances, but mortgage loan servicers donât consider these beyond your control. Note that you can still qualify for a conventional loan if you put down less than 20 percent.

In many cases, PMI companies impose stricter standards than Fannie Mae or Freddie Mac. Someone with a foreclosure a year ago who has a credit score of at least 550 and has an otherwise clean credit history can get a loan, says Privlo founder Michael Slavin. The rules for getting a conventional mortgage after you have foreclosed is that you wait 7 years. However, if there were “extenuating circumstances”, such as a job loss, or something else out of your control, this may be reduced to only 3 years. Please keep in mind that non-prime loans require larger down payments, and have higher interest rates than conventional and government-backed loans. Therefore, it is important that you learn about all of your options, so that you can make an educated decision about what program makes most sense for you.

Be prepared to document everything finance-related in your postforeclosure life, advises Rodriguez. That includes pay stubs, bank and brokerage statements, and tax returns. Lenders will ask for this paperwork to verify everything you put on your mortgage application as a precaution to avoid another potential foreclosure. Check your credit and determine what options -- conventional, government, non-prime, and more -- are available to you. Past foreclosures make you statistically more likely to default on a loan. Aspiring homeowners who are interested in applying for an FHA loan will also need to invest in mortgage insurance.

The lender is looking for proof the circumstances that caused the foreclosure are well behind you and are not likely to be repeated. For example, if you had a medical emergency, incurred high hospital bills and missed work, but you are now recovered, then there’s a good chance you could be approved as a home buyer. But, if you had gambling problems and you’re still regularly visiting the casino, you won’t be approved. "A recent foreclosure doesn't mean that you can't get a mortgage," Slavin says. "There are alternative lenders like Privlo who work with credit rebuilders and understand that there are people who deserve a second chance at homeownership."

Comments

Post a Comment